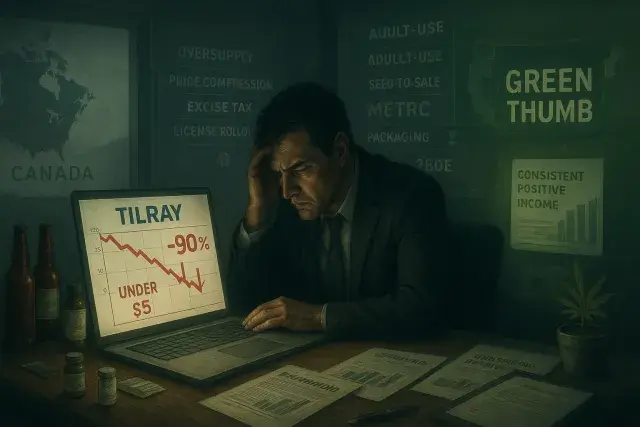

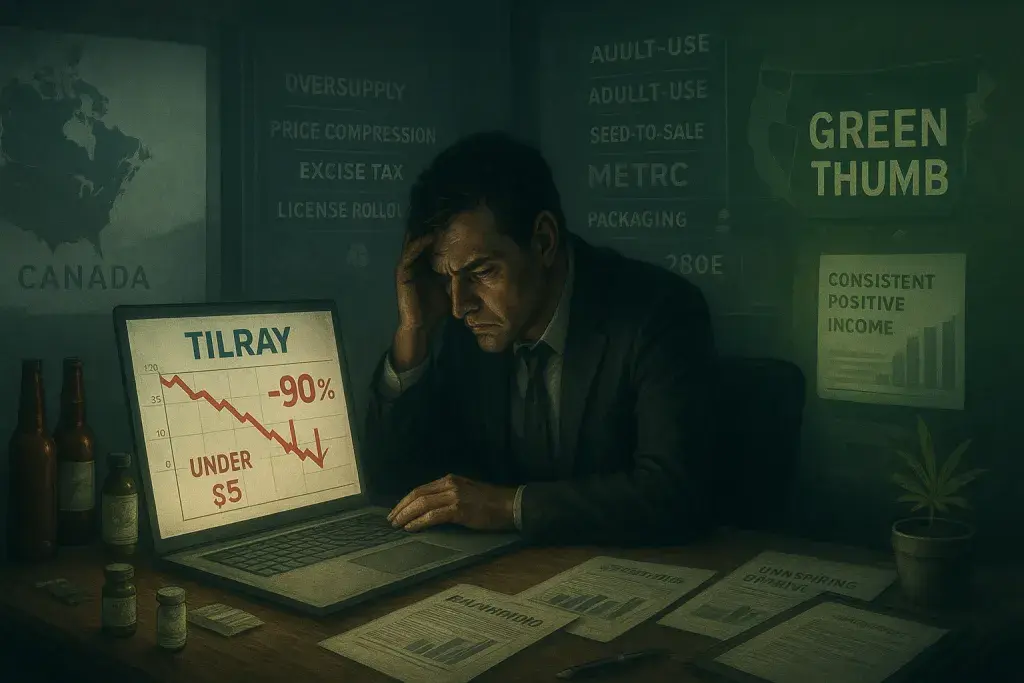

Tilray Brands has shed more than 90% of its value over the past five years, with shares trading at just under $5. For cannabis investors who have been watching the company's trajectory, that number alone tells a complicated story - one about the limits of market leadership in a sector where being number one doesn't necessarily translate into profitability. Tilray holds a top position in Canadian recreational cannabis, yet the company remains unprofitable, and its organic revenue growth has been, at best, uninspiring.

The diversification argument is where things get more interesting - and more contested. Tilray has moved well beyond cannabis, building a portfolio that includes craft brewing (it ranks as the fourth-largest craft brewer in the U.S.), hemp-based wellness products, and pharmaceutical operations. That breadth is a real structural shift, not just a press-release pivot. Whether it's enough to offset years of weak cannabis performance is another question entirely. Operators in regulated cannabis markets who want to understand how market structure affects business performance across different state frameworks can see how it works in one of the country's most closely watched adult-use environments. The broader point stands: diversification looks better on a slide deck than it does on an income statement until the numbers actually improve.

The recent reclassification of certain cannabis products from Schedule I to Schedule III is a genuine regulatory development, not a minor footnote. Products that contain marijuana and carry FDA approval, along with state-regulated cannabis products, now sit in a category that acknowledges some degree of medical utility and lower abuse potential. That matters for medical research, for pharmaceutical applications, and - over a longer horizon - for how institutional capital might look at the sector. Tilray has a footprint in pharmaceuticals, so the Schedule III shift isn't irrelevant to its positioning. Here's the catch, though: regulatory progress in cannabis has consistently disappointed investors who priced in the optimistic scenario too early.

What Canada's Experience Actually Teaches

Canada is the instructive case. Adult-use legalization arrived with enormous expectations - and then ran into production oversupply, persistent price compression, provincial distribution bottlenecks, and a gray market that refused to disappear. Regulatory frameworks that looked permissive on paper turned out to carry significant operational constraints in practice. Excise tax structures squeezed margins at the licensed producer level. Retail license rollouts moved unevenly across provinces, creating supply chain mismatches that took years to sort out. Tilray competed in that environment and still couldn't generate consistent profits. That's not just a Tilray problem - it reflects how punishing regulated cannabis markets can be for operators of any size - but it's a fair lens for evaluating what a more favorable U.S. regulatory posture might actually deliver.

The U.S. market, even if federal policy continues to soften, will not be a clean runway. State-by-state adult-use frameworks come with their own compliance overhead: seed-to-sale tracking requirements, METRC integrations, packaging and labeling mandates, potency testing and COA documentation, social equity obligations, and excise tax structures that vary significantly by jurisdiction. Any large operator - including a well-capitalized one - entering or expanding in the U.S. market faces that patchwork in full. The competitive field will be crowded, and companies with established dispensary networks, strong POS infrastructure, and deep wholesale relationships will have real advantages over those trying to build those systems from scratch.

The Comparison That Matters for Cannabis Investors

Among cannabis-focused companies with actual U.S. operations, Green Thumb Industries stands out as the more compelling business case. It operates as a multi-state operator with consistent profitability - a distinction that is genuinely rare in this sector - and has a strong presence in high-volume markets including Florida. That's not a small thing. Profitable multi-state operators have demonstrated they can manage the full operational stack: retail compliance, inventory management, wholesale pricing strategy, and the tax burden that comes with 280E, which disallows standard business deductions for companies trafficking in federally controlled substances. Green Thumb has done that work. The financial results reflect it.

Tilray, by contrast, is asking investors to bet on a turnaround story built on diversification into adjacent industries and a regulatory environment that may - eventually - become more favorable. That's not an impossible thesis. But cheap shares aren't the same thing as undervalued shares. A stock trading near multi-year lows is only a value opportunity if the business has a credible path to improved performance. Right now, Tilray's cannabis operations remain a drag, and the company's non-cannabis segments haven't yet demonstrated they can compensate decisively. Until the income statement shows something materially different, the argument for Tilray over a consistently profitable operator is a difficult one to make with a straight face.